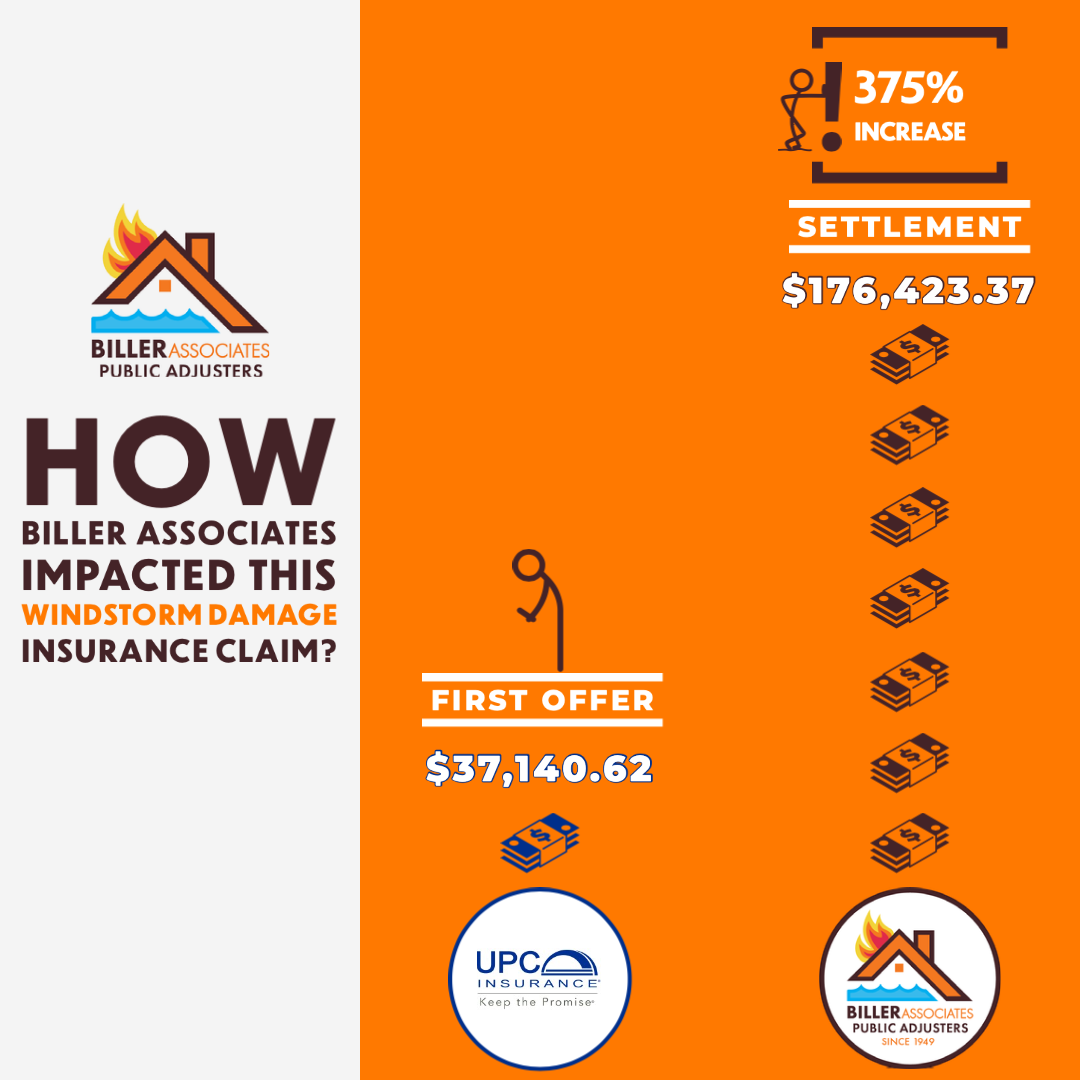

If you suspect your roof was damaged due to wind, hail, fallen debris or trees, it is important that you call Biller Associates Public Adjusters to help maximize your insurance claim.

In nearly every situation, when an insurance adjuster is called, their inspection is limited in their effort to find damages (if they show up at all). Lets face it, the insurance industry is a for-profit industry and their goal is report profits so the NASDAQ number is shiny and pretty.

With a Public Adjuster, we work for YOU, NOT the insurance company. As a matter of fact, we take care of everything and we fight for you every step of the way. Not only will we find damages, we use the latest technologies (https://www.billerassociates.com/technology) to document the damages and to report them to your insurance company for proof and accuracy.

We put together information to assist you with common roof damage insurance claims.

Factors that Affect Your Roof Insurance Claim

There are 5 common factors that will influence your roof insurance claim:

- How many homeowners insurance claims have you filed in the past 5 years?

- What is your deductible?

- How bad is the roof damage?

- What is the value of your roof? (Do you have replacement cost coverage?)

- How competent are you alone in getting your claim approved?

If you answered more than 1 claim in the past 5 years

It is not uncommon for a homeowner to file a claim or two every 10 years, but if you are the type to file a claim or two every five years, you are likely paying crazy rates and should consult with a Public Adjuster before filing any future claims.

What is your deductible?

Before you ever file a claim for your roof, make sure you have proper coverage, call Biller Associates Public Adjusters and we will help you determine if the damage outweighs the deductible.

For example, if the damage is only 1,800 and your deductible is $2,000, it may make sense to pay out of pocket, otherwise your rates will increase.

How much is your roof worth?

Just like anything, your roof value depreciates. A 10 year old roof that was rated for 20 years is not worth what it was when it was first installed.

As we review your policy with you, we will check to see if you have ACV or RCV coverage. ACV simply means “Actual Cash Value” and RCV means “Replacement Cost Value”.

Most people opt for ACV as the monthly premiums are lower, unfortunately, they will only pay for the value of the roof in its current state.

Regardless, we are experts in maximizing claims and whether you think your roof is in awful shape, let us handle the negotiation.

How competent are you on you insurance policy and should you hire us?

Simply said, it will pay to have an experience Public Adjuster on your side. Working with insurance companies is stressful and we take care of everything and we work for YOU, NOT the insurance company.

Here is the Most Important Part

A new roof is one of the most expensive claims you will have for your home. When wind, debris or trees cause damage to your roof, your first phone call should be to Biller Associates Public Adjusters. We will call your insurance company, we will document the damages and we will maximize your claim.

Call Biller Associates Public Adjusters at 203.234.9865